If you have opened a health insurance renewal letter lately and felt shocked by the price, you are not alone. Premiums in New Zealand are going up fast, much faster than the cost of groceries or petrol. And unlike a lot of price rises, this one is not going away anytime soon.

The good news is there are real, understandable reasons behind it. Once you know what is driving the cost, you can make much smarter decisions about your cover. This article explains what is happening, why New Zealand is actually one of the worst-affected countries in the world, and what your options are.

Just How Much Have Premiums Gone Up?

Let’s start with the numbers, because they are pretty eye-opening.

According to Stats NZ, health insurance premiums rose nearly 20% in a single year (to September 2025).[1] One RNZ investigation found a healthy young person had their premiums go up by 25% in twelve months.[2] Over the same period, everyday inflation in New Zealand sat at around 3%.[3]

In plain terms: health insurance costs went up about seven times faster than the price of everything else in your life. That is a huge gap.

The Financial Services Council says that 1.35 million New Zealanders (roughly one in four people) hold health insurance. That number actually grew by 3.3% between March 2024 and 2025.[4] Even with higher premiums, more Kiwis are choosing to take out cover. That tells you something important: people are seeing how stretched the public system is, and they are voting with their wallets.

health insurance premium increase year-on-year (Stats NZ, September 2025)[1]

The Main Culprit: Medical Inflation

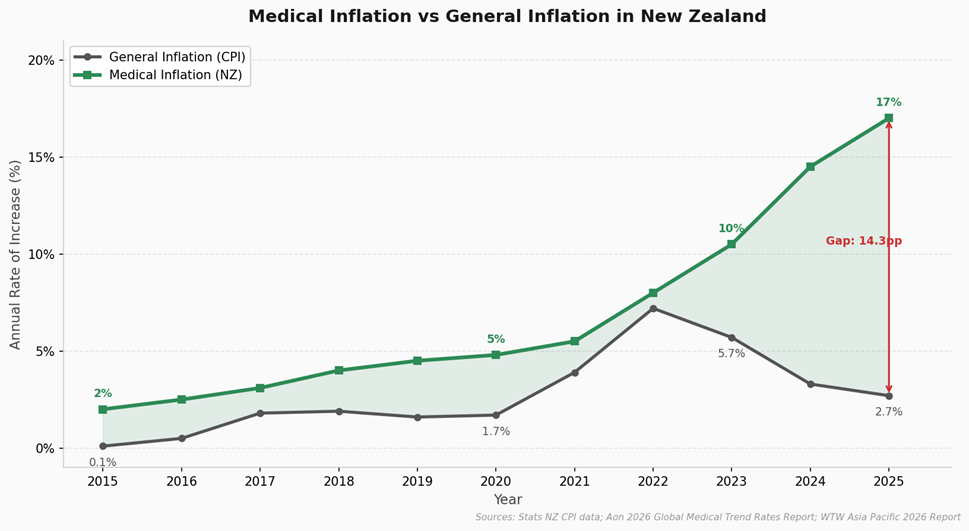

There is a specific kind of inflation that affects health insurance, and it is very different from general inflation. It is called medical inflation, and it tracks how much more expensive healthcare itself is getting: operations, specialist visits, scans, and medicines.

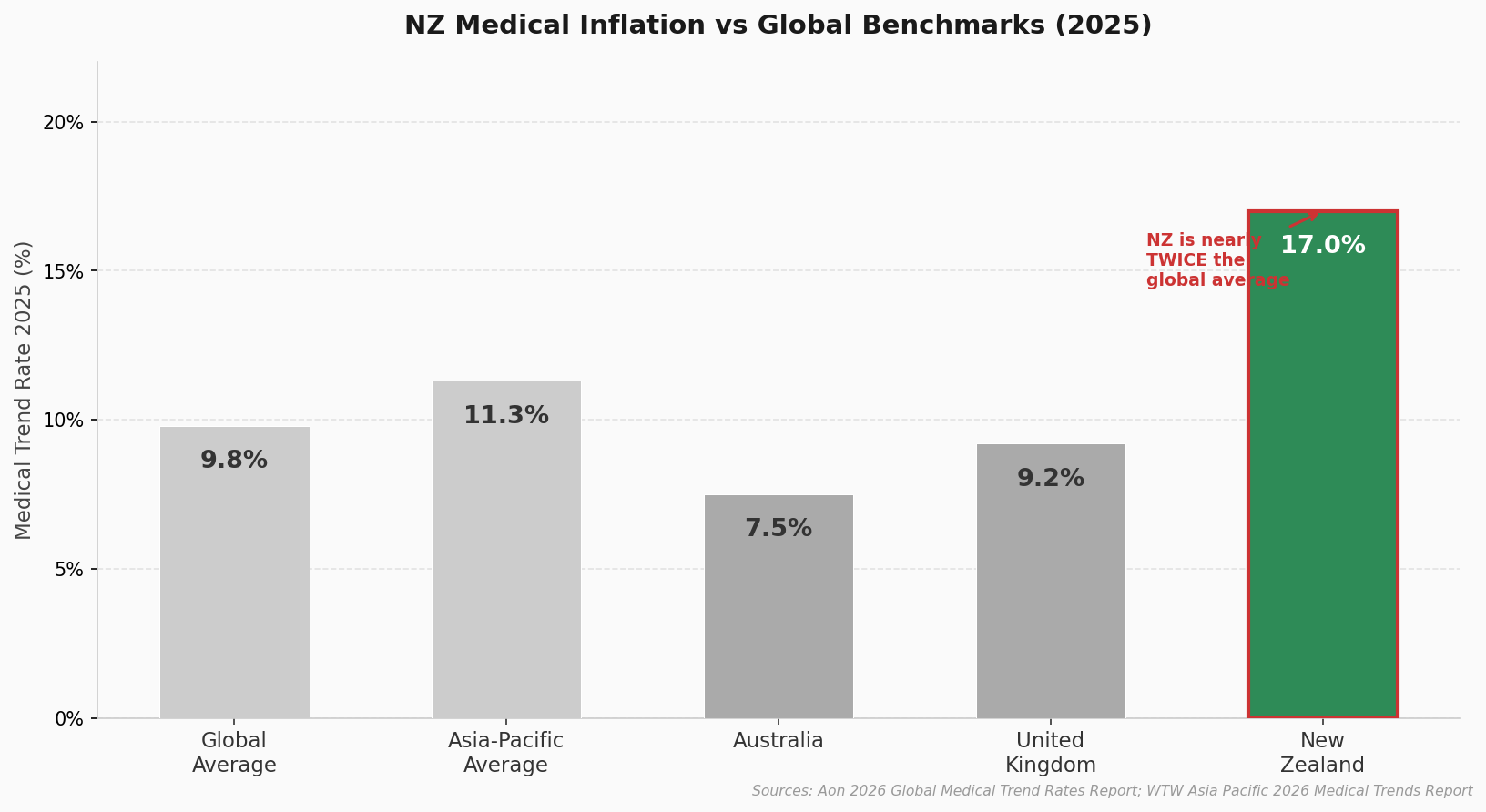

Steve Gregory, who leads employee health and benefits at Aon New Zealand, puts the figure at 17% medical inflation in 2025, up from 10% the year before.[5] The global average is 9.8%, and across Asia-Pacific it is 11.3%. New Zealand is running at nearly twice the world average.

Looking ahead, Aon’s 2026 Global Medical Trend Rates Report forecasts New Zealand’s healthcare costs will rise by another 18% in 2026,[6] while WTW (a major global insurance research group) expects the world average to be around 10.3%.[7] We are nearly double what the rest of the world is experiencing.

When the underlying cost of healthcare goes up this much, insurers have to charge more to cover their claims. It is that simple.

The Public System Is Struggling, and That Pushes Costs Into Insurance

Here is something a lot of people do not realise: when the public health system gets slower, it directly pushes up the cost of private health insurance.

Think about it this way. If you cannot get a knee operation through the public hospital for two years, and you have health insurance, you use your insurance to get it done privately. Multiply that across hundreds of thousands of people, and insurance companies end up paying for far more claims.

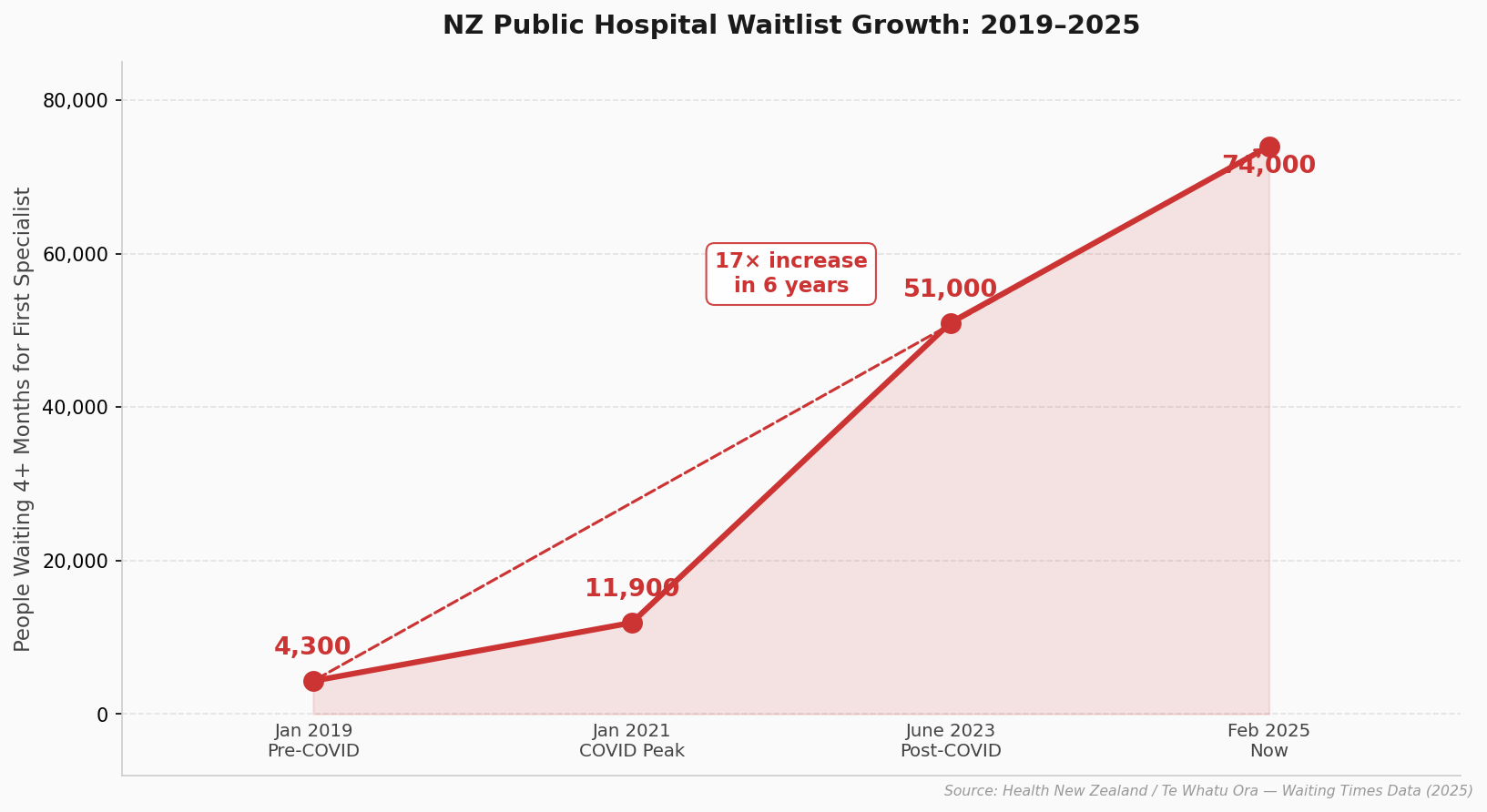

As of February 2025, more than 74,000 New Zealanders had been waiting longer than four months just to see a specialist for the first time.[8] A further 37,000+ were waiting longer than target times for actual treatment. The specialties with the longest queues include orthopaedics, eye surgery, ear, nose and throat, and general surgery.

New Zealand’s public health spending has stayed below 7% of GDP since at least 2010, while similar countries spend more.[8] A 2024 OECD study found that only 46% of New Zealanders are satisfied with their healthcare system, compared to an OECD average of 52%.[5] That gap between what the public system can provide and what people need is being filled by private insurance, and someone has to pay for it.

The COVID Catch-Up

During New Zealand’s lockdowns in 2020 and 2021, thousands of operations and appointments were postponed. People put off knee replacements, delayed cancer checks, and skipped specialist appointments.

The number of patients waiting more than four months for treatment tripled, from around 4,300 in January 2019 to over 11,900 by January 2021.[8] When restrictions lifted, all of those delayed people started using the health system at once. Insurance companies started paying out much higher claim volumes from 2022 onwards, right when medical costs were also accelerating. That double hit squeezed insurer finances hard.

New Zealand Is Getting Older

About 17% of New Zealand’s population is currently aged 65 or over.[8] That is forecast to rise to around 24% (about 1.5 million people) over the next 30 years.

Older people, on average, need more healthcare: more specialist appointments, more operations, more medications. As the insured population ages, insurers pay out more, even if nothing else changes.

This is a long-term, structural shift that will continue to push premiums higher, regardless of what happens with medical costs or the public health system.

The Pharmac Gap: Medicines New Zealand Does Not Fund

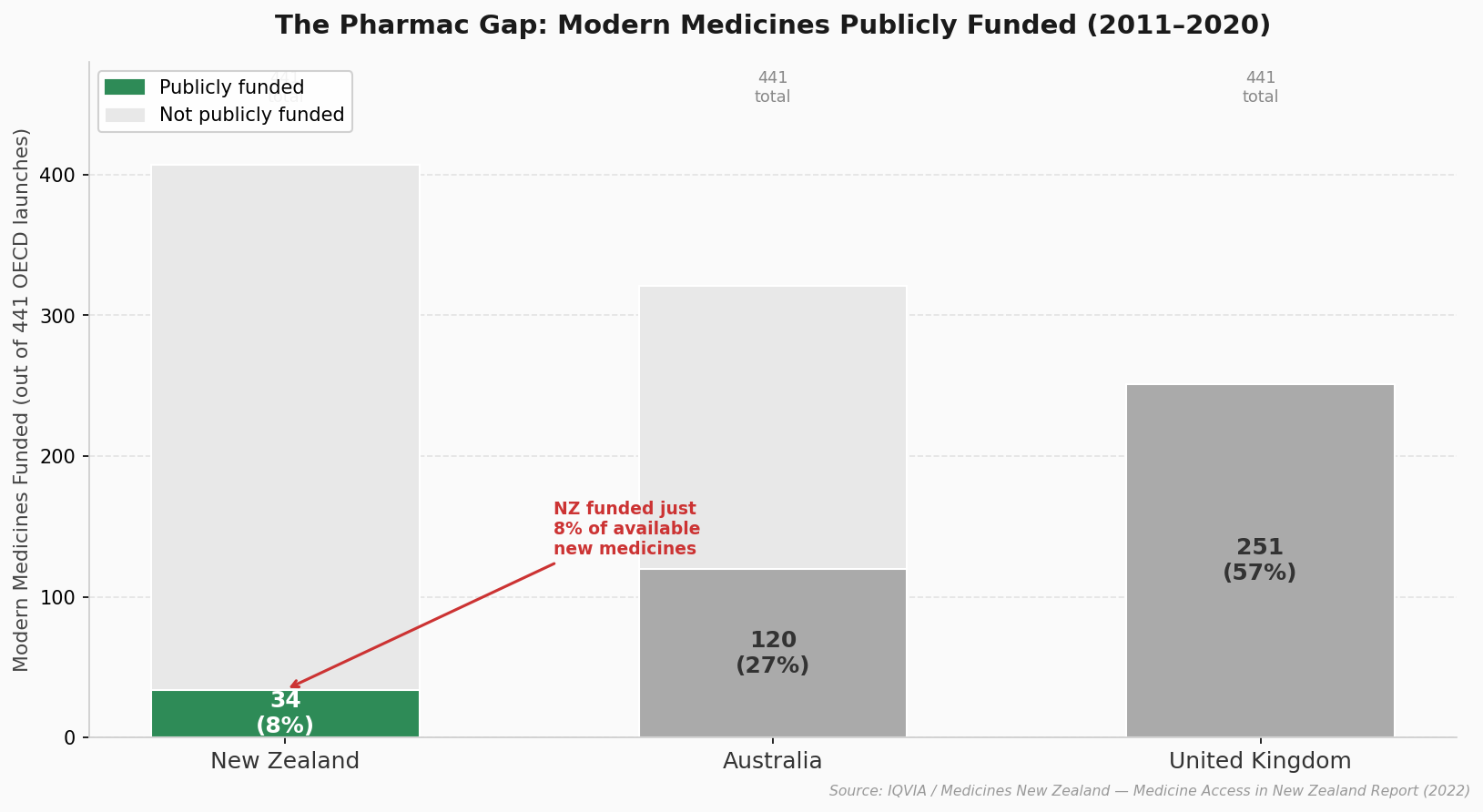

In New Zealand, a government agency called Pharmac decides which medicines are publicly funded. This system helps keep drug costs down, but it also means New Zealand funds far fewer medicines than comparable countries.

Between 2011 and 2020, only 10% of new cancer treatments available across OECD countries were accessible in New Zealand.[9] Out of 441 modern medicines launched globally, only 34 were publicly funded here. By comparison, Australia funded 120 and the UK funded 251.[9]

When a cancer drug is not funded by Pharmac, patients who have private health insurance may be able to claim it through their policy. But some of these drugs cost hundreds of thousands of dollars per year. Around 300 funding applications are still sitting in Pharmac’s queue waiting for approval.

This puts real pressure on insurance claim costs, particularly for policies that include non-Pharmac drug cover.

The Insurers Are Actually Running at a Loss

Here is a fact that surprises most people: health insurers in New Zealand have not been profiting from this situation. They have been losing money.

The Reserve Bank of New Zealand (RBNZ) has stepped up its oversight of the health insurance sector, warning that sustained operating losses have reduced insurers’ financial buffers by nearly 40% over the past two years.[10]

The RBNZ stated in its Financial Stability Report that premium increases will be needed to restore profitability, so that the sector can sustainably provide services to policyholders and support the wider health system.

In other words, the Reserve Bank is not warning that insurers are charging too much. It is warning they may not be charging enough to survive long-term.[10] Insurers have been absorbing the losses, drawing down their reserves, and hoping medical inflation would ease. It has not. Now they are raising premiums, and in some cases narrowing what is covered, to stay financially healthy.

What Can You Actually Do About It?

Rising premiums put people in a tough spot. The temptation is to cancel cover to save money. But the people most likely to do that are healthy, younger policyholders who rarely claim. When they drop out, the pool of insured people skews older and sicker, which pushes premiums up even further for everyone who stays. It is a cycle that can feed on itself.

The smarter move is to review your policy rather than cancel it. There are often real savings to be found by adjusting your excess (the amount you pay before insurance kicks in), removing cover you might not need, or switching to a policy that is better value for your situation.

The catch is that comparing health insurance policies is genuinely complicated. Benefits, exclusions, excess levels, and non-Pharmac cover all vary significantly between providers, and the differences are not always obvious.

The Bottom Line

Health insurance premiums in New Zealand are rising because the underlying cost of healthcare is rising faster here than almost anywhere else in the world. That is being driven by medical inflation, an ageing population, a wave of deferred treatment from the COVID years, a public health system under serious pressure, and a medicines funding gap that leaves many Kiwis relying on private insurance for the most expensive treatments.

The Reserve Bank is now watching the sector closely. Premiums are likely to stay elevated for the foreseeable future. The question is not whether this is happening. The question is how to handle it sensibly.

If your renewal is coming up, or you have not reviewed your policy in a while, get in touch for a no-obligation review. A few minutes could save you hundreds of dollars a year while making sure you are still properly protected.

Get a no-obligation policy review

We help you find better value without sacrificing protection.

Get in touchHow Do We Fix It?

The factors below each point in one direction: slowing down the rate of premium increases. None of them are quick fixes. All of them matter.

1. Younger People Need to Sign Up

Health insurance works like a pool. The more healthy, low-claim people in it, the lower the cost for everyone. Right now, that pool is skewed heavily toward older New Zealanders. The Ministry of Health’s 2023/24 New Zealand Health Survey confirms that the 45-54 age group has the highest coverage rate at 45.2%, while young adults in their 20s and 30s are significantly underrepresented.[11] That imbalance matters because people over 50 make three to four times more claims than those under 35.[12]

The good news: a 25-year-old pays around $100 per month for comprehensive hospital cover with a $500 excess. That is genuinely affordable. The sooner young people join, the more they protect their own future premiums and the lower they help keep premiums for everyone else.

2. Fund More Cancer Drugs

This is a Pharmac and government issue, not just an insurance one. Between 2011 and 2020, New Zealand publicly funded only 34 modern medicines out of 441 launched across OECD countries. Australia funded 120. The UK funded 251.[9] On cancer specifically, New Zealand funded just 10% of new cancer treatments launched across OECD nations in that same period.[13]

The flow-on effect hits insurers directly. When a drug is not publicly funded, patients who can access private health insurance claim it through their policy instead. The more treatments that sit outside the public system, the more cost that flows through private insurance, and the higher premiums climb. The 2024 government funding boost (an extra $604 million over four years for 66 new medicines) was a step forward.[13] But the gap between New Zealand and comparable countries is still wide, and according to Medicines New Zealand, it is actually getting worse, not better.[14]

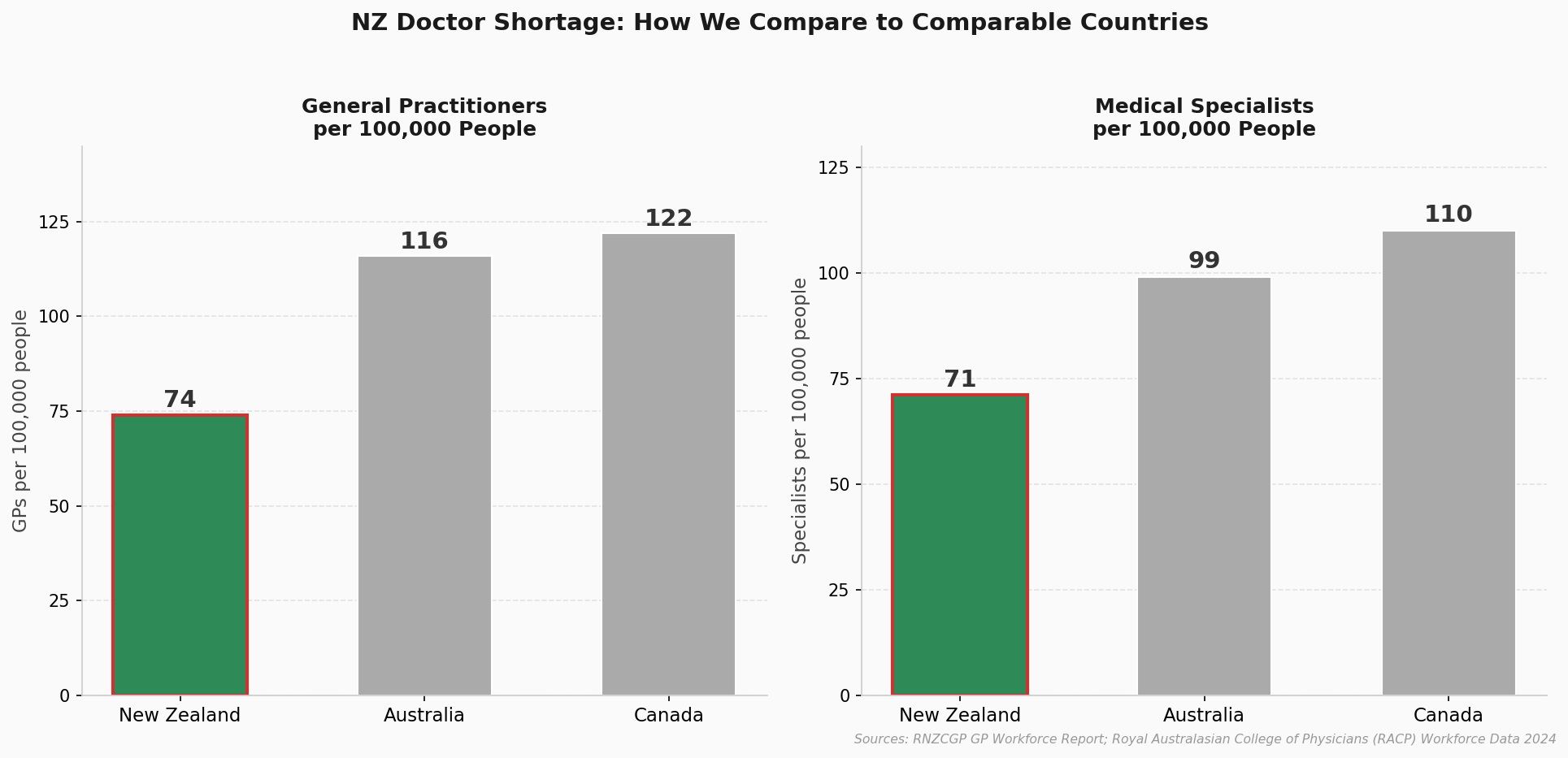

3. Train and Retain More Doctors

New Zealand has about 74 GPs per 100,000 people. Australia has 116. Canada has 122.[15] The Royal Australasian College of Physicians puts our specialist ratio at just 71 per 100,000, compared to 99 in Australia.[16] The result is a system under severe strain. In 2024, 36% of general practices were not accepting new patients.[17] Government projections put the shortfall at over 5,000 doctors within a decade.[18]

Fewer doctors means longer public wait times. Longer wait times push more people into private care. More private care means more insurance claims. More claims mean higher premiums. The link between GP supply and what you pay for health insurance is real.

4. Grow Employer-Sponsored Cover (And Perhaps Remove FBT on It)

Employer group schemes are one of the most effective ways to bring younger, healthier people into the insured pool. When an employer subsidises cover, employees who would never have bought health insurance individually end up enrolled. That broader, younger membership base spreads risk more evenly and puts downward pressure on premiums over time.

The obstacle? In New Zealand, employer-paid health insurance is subject to Fringe Benefit Tax (FBT) at up to 49.25%.[22] That is a significant cost for employers considering offering fully subsidised plans. Compare this to our peers: in the United States, employer-paid health insurance premiums are completely exempt from federal tax.[19] In Australia, group health insurance policies where the employer is the policyholder can generally be exempt from FBT.[20] Even in the UK, while employer-provided health benefits are taxed, they are assessed at the employee’s marginal income tax rate rather than a punishing employer-side rate.[21]

A targeted FBT exemption for fully employer-subsidised health insurance plans would make New Zealand more competitive with the countries we compare ourselves to, encourage more businesses to offer cover as a workplace benefit, and help widen the insured pool. It is, perhaps, worth a conversation.

5. Invest in the Public System

Private health insurance does not operate in a vacuum. It exists to fill the gaps left by the public system. The bigger those gaps grow, the more work private insurance must do, and the more it costs. New Zealand’s pharmaceutical spend sits at just 0.38% of GDP. The OECD average is 1.41%.[13] That is not a rounding error. That is structural underinvestment that flows directly into the claims experience of every insurer in this country and, ultimately, into your renewal notice.

This article is general information only and does not constitute personalised financial advice. Blake Dowman is a Registered Financial Adviser (FSP 1007984) operating under AIA Thrive Limited FAP. For advice tailored to your circumstances, please contact us directly.

References

- [1]Statistics New Zealand. (2025). Consumers Price Index: September 2025 quarter. https://www.stats.govt.nz/information-releases/consumers-price-index-september-2025-quarter/

- [2]Kerr-Bell, S. (2025, October). 'Healthy, young' but medical insurance premiums rise 25 percent in a year. RNZ News. https://www.rnz.co.nz/news/business/577123/healthy-young-but-medical-insurance-premiums-rise-25-percent-in-a-year

- [3]Statistics New Zealand. (2025). Annual inflation at 3.0 percent in September 2025. https://www.stats.govt.nz/news/annual-inflation-at-3-0-percent-in-september-2025/

- [4]Financial Services Council New Zealand. (2025). Health insurance coverage statistics, March 2024 to 2025. https://www.fsc.org.nz/topics/health-insurance

- [5]Gregory, S. (2025). How much health insurance costs could surge in 2026. Stuff. https://www.stuff.co.nz/money/360915717/after-36-years-paying-premiums-pensioner-faces-another-health-insurance-hike-how-much-her-costs-and

- [6]Aon. (2025). 2026 Global Medical Trend Rates Report. https://www.aon.com/en/insights/reports/the-global-medical-trend-rates-report

- [7]WTW. (2025). 2026 medical trend rates insights: Asia Pacific. https://www.aon.com/apac/insights/blog/default/2026-medical-trend-rates-insights-asia-pacific

- [8]Health New Zealand | Te Whatu Ora. (2025, February). Waiting times data. https://www.tewhatuora.govt.nz/our-health-system/data-and-statistics/waiting-times/

- [9]IQVIA, commissioned by Medicines New Zealand. (2021). A decade of modern medicines: An international comparison 2011 to 2020. https://www.policywise.co.nz/resources/non-pharmac-drugs

- [10]Reserve Bank of New Zealand. (2025). Financial Stability Report. https://www.rbnz.govt.nz/hub/publications/financial-stability-report

- [11]Ministry of Health. (2024). Annual update of key results 2023/24: New Zealand Health Survey. https://www.health.govt.nz/publications/annual-update-of-key-results-202324-new-zealand-health-survey

- [12]InsureNZ. (2025). Health insurance cost NZ 2025: Complete pricing guide by age. https://insurenz.co.nz/blog/health-insurance-cost-nz-2025

- [13]Pharmac. (2024). Cancer and other medicines funded from 2024 Budget. https://www.pharmac.govt.nz/medicine-funding-and-supply/funding-cancer-medicines

- [14]Medicines New Zealand. (2025, October). Australia funding more medicines faster than Aotearoa. As reported by RNZ. https://www.rnz.co.nz/news/national/574799/australia-funding-more-medicines-faster-than-aotearoa-report-finds

- [15]Royal New Zealand College of General Practitioners. (n.d.). GP future workforce requirements report highlights. https://www.rnzcgp.org.nz/news/college/gp-future-workforce-requirements-report-highlights/

- [16]Royal Australasian College of Physicians. (n.d.). Workforce data shows physician shortages across Aotearoa New Zealand. https://www.racp.edu.au/news-and-events/media-releases/workforce-data-shows-physician-shortages-across-aotearoa-new-zealand

- [17]RNZ. (2025, January). Staff shortages key driver as more general practices turn away new patients. https://www.rnz.co.nz/news/national/540200/staff-shortages-key-driver-as-more-general-practices-turn-away-new-patients

- [18]NZ Herald. (2023, July). Government launches health workforce plan; nearly 13,000 extra nurses and over 5,000 doctors needed within a decade. https://www.nzherald.co.nz/nz/politics/government-launches-health-workforce-plan-nearly-13000-extra-nurses-and-over-5000-doctors-needed-within-a-decade/K5GHGVYMMNA4HOWWN5DBMLFUSE/

- [19]Internal Revenue Service. (2025). Publication 15-B: Employer's tax guide to fringe benefits. https://www.irs.gov/publications/p15b

- [20]Deloitte New Zealand. (2024, September). Fringe benefit tax: A trans-Tasman guide. https://www.deloitte.com/nz/en/services/tax/perspectives/september-2024-fringe-benefit-tax-a-trans-tasman-guide.html

- [21]HM Revenue & Customs. (n.d.). Tax on company benefits. https://www.gov.uk/tax-company-benefits

- [22]RNZ. (2025). Health insurance crunch prompts calls for fringe benefit tax break. https://www.rnz.co.nz/news/business/566943/health-insurance-crunch-prompts-calls-for-fringe-benefit-tax-break